UK Statutory Residence Test: What Travelers Need to Know

A practical explainer of what the UK's tax-residence test is trying to determine, why it is not just a simple 183-day rule, and where prior residence, ties, and HMRC guidance matter.

Last verified: June 2026

What This Page Explains

This page explains the core mental model behind the UK's Statutory Residence Test for people whose UK travel dates may affect whether they are treated as UK resident for tax purposes.

- what the Statutory Residence Test is trying to determine

- why the UK question is not just a simple annual 183-day threshold

- how the automatic overseas tests, automatic UK tests, and sufficient ties test work at a high level

- why prior residence status and the strength of your UK ties matter

- where this explainer stops and where HMRC guidance or professional advice matters more

It is not tax advice, and it does not tell you whether you should file a UK return in a certain way. The aim is to give you a trustworthy framework before you rely on casual shorthand, half-remembered travel dates, or a spreadsheet that was never built for multi-year residence questions.

The key boundary: the Statutory Residence Test is a UK tax-residence framework. It is not the same thing as visitor permission, the UK Standard Visitor assessment, or a general idea of whether you "live" in the UK.

What the Statutory Residence Test Is Trying to Determine

At a high level, the Statutory Residence Test, usually shortened to SRT, is the UK's framework for deciding whether you are UK resident for a tax year. HMRC's guidance treats each tax year separately, so the question is year-specific rather than permanent.

The test looks at time spent in the UK, work patterns where relevant, and your connections to the UK. That matters because UK residence status can affect the scope of your UK tax position and the next questions that need to be asked.

The real question is not "have I spent a lot of time in the UK?" in a casual sense. The real question is whether your days, work pattern, home position, and ties are enough to make you UK resident under the SRT for the relevant tax year.

Why It Is Not Just a Simple 183-Day Threshold

People often reduce UK tax residence to "183 days in the UK means resident." That shorthand is incomplete.

- 183 days is only one automatic UK test. It is decisive if you reach it, but it is not the whole framework.

- The UK works by tax year, not calendar year. A pattern that looks harmless in January-to-December terms can still matter when the relevant year runs differently.

- You can be resident below 183 days. A UK home, full-time work in the UK, or enough UK ties can matter even when you never reach 183 days.

- You can also be clearly non-resident under automatic overseas tests. The analysis is not just about proving residence.

- Day counting itself has rules. HMRC generally counts UK presence by where you are at the end of the day, but deeming and exceptional-circumstances rules can change the practical total.

So the serious UK question is not just "did I cross 183 days?" It is "which part of the SRT applies to me, how are my days counted for this tax year, and do my prior years and UK ties change the answer?"

The practical consequence: someone can stay below 183 UK days and still have a real UK tax-residence question, especially if they were recently UK resident or still have strong UK connections.

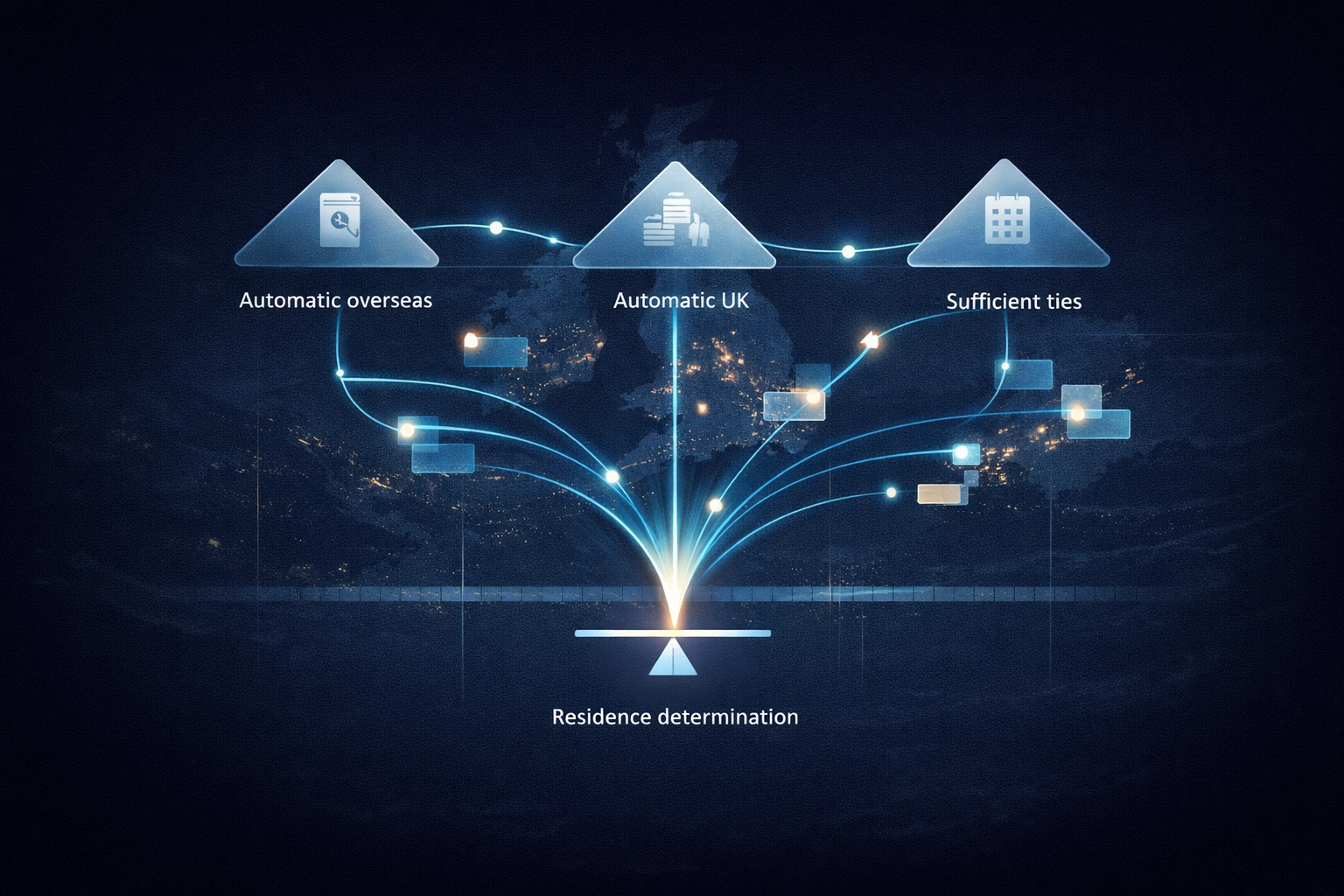

How the Three-Part Structure Works at a High Level

HMRC describes the SRT as a sequence. You first check the automatic overseas tests, then the automatic UK tests, and only then the sufficient ties test if neither side has already decided the year.

Automatic Overseas Tests

The automatic overseas tests are the part of the framework that can make you non-UK resident for the tax year without needing to go into the ties analysis.

- If you were UK resident in one or more of the previous three tax years, spending fewer than 16 days in the UK can be enough for automatic non-residence.

- If you were not UK resident in any of the previous three tax years, the low-day threshold is different: fewer than 46 UK days.

- There is also a full-time overseas work test with its own UK day and UK workday limits.

The important point is conceptual: prior residence already matters here. The SRT is not built on one identical threshold for everyone.

Automatic UK Tests

If no automatic overseas test applies, you then check whether you are automatically UK resident.

- The clearest automatic UK test is 183 days or more in the UK in the tax year.

- A UK home can also create automatic residence under detailed conditions, even below 183 days.

- Full-time work in the UK over a qualifying period can also create automatic residence.

This is why "under 183" is not a safe shorthand. The home and work tests are real tests, with detailed conditions, and they can matter before the day count reaches the headline number people remember.

Sufficient Ties Test

If neither side is decided automatically, the SRT moves to the sufficient ties test. This is where many practical edge cases sit.

At a high level, HMRC looks at your UK ties, such as family, accommodation, work, and prior time spent in the UK. If you were UK resident in one or more of the previous three tax years, you may also need to consider the country tie.

The key logic is simple even though the rules are detailed: the more UK ties you have, the fewer UK days you can spend there before becoming resident. HMRC's own tables are stricter for people who were recently UK resident than for people who were not.

- For someone resident in one or more of the previous three tax years, the sufficient ties table can start as low as 16 to 45 UK days if that person has four ties.

- For someone not resident in any of the previous three tax years, the sufficient ties tables do not start until 46 UK days and generally require more ties.

That is the real reason prior residence status matters so much. It changes the table you use, and therefore changes how quickly a moderate number of UK days becomes tax-relevant.

Tracking this yourself? AtlasDays keeps a private, dated travel record on your iPhone and counts the days that matter — visa limits, residency thresholds, and country totals. Get the app →

Common Misunderstandings and False Assumptions

- Assuming the UK uses a calendar year for this test. The SRT works by UK tax year, not January to December.

- Assuming under 183 days ends the analysis. It does not, because the home test, full-time UK work test, and sufficient ties test can still matter.

- Assuming visitor rules and tax residence are the same question. A Standard Visitor stay pattern and UK tax residence are separate legal frameworks.

- Assuming ties are vague or informal. HMRC gives each tie its own conditions; this is not just a gut-feel exercise about whether you "still seem connected" to the UK.

- Assuming every UK touchpoint counts the same way. HMRC generally counts a day by presence in the UK at the end of the day, but there are additional deeming and exceptional-circumstances rules.

- Assuming the SRT alone answers every UK tax question. Split year treatment, dual residence, treaty issues, and fact-specific advice can still matter after the core SRT analysis.

What Changed in April 2025: Non-Dom Abolition and the FIG Regime

The SRT rules themselves have not changed. The test you apply to count days, check ties, and decide residence status is the same as before. What changed significantly in April 2025 is what happens once you are determined to be UK resident.

From 6 April 2025, the remittance basis of taxation for non-domiciled individuals was abolished. In its place, HMRC introduced the Foreign Income and Gains (FIG) regime. Under the FIG regime, individuals who have been non-UK resident for at least 10 consecutive tax years immediately before becoming UK resident can elect to shelter their foreign income and gains from UK tax for their first four tax years of UK residence. After that four-year window closes, their foreign income and gains become subject to UK tax in the usual way.

This change matters for anyone who:

- has recently become UK resident after a long period overseas

- previously relied on the remittance basis for offshore income or gains

- is planning a return to the UK and has foreign assets or income streams

- is in the middle of the four-year FIG window and needs to understand when it closes

For those cases, the SRT question (am I UK resident?) is still step one. But the tax consequence of being UK resident is now materially different from what the old non-dom rules produced. If prior residence analysis or offshore income is part of your picture, this is an area where professional advice matters more than a general article.

HMRC's current guidance on the FIG regime is in RDR1 and the updated internal manual sections that now carry the "Residence and FIG Regime Manual" label.

Practical Caution and HMRC/Professional-Advice Boundary

This page is a general explainer, not a substitute for official HMRC guidance or case-specific professional advice.

- For the structure of the test itself, start with HMRC's RDR3 Statutory Residence Test guidance.

- For the broader effect of UK residence status and HMRC's general residence guidance, use RDR1.

- For technical points on day counting and ties, HMRC's manual sections on the deeming rule and sufficient ties tables are more precise than any short explainer can be.

- HMRC updated RDR3 on 11 June 2026 with temporary non-residence material, so use the current version if your facts include leaving the UK and later returning.

- If your facts involve arriving in or leaving the UK mid-year, dual residence, treaty tie-breakers, substantial UK work, or a meaningful amount of tax at stake, this is the point where professional advice matters more than a general article.

That boundary is important because the SRT is structured and statutory, but it is not a toy rule. Once you are asking whether a home qualifies, whether a tie exists, whether the deeming rule changes your day count, or whether split year treatment applies, you are already beyond headline-rule territory.

When Manual Tracking Starts to Break Down

Manual counting is manageable when you had one obvious UK stay and clean records. It breaks down when you have:

- repeated UK trips spread across multiple tax years

- older arrival and departure dates that were never cleaned up properly

- same-day travel, late-night arrivals, or patterns where the end-of-day rule starts to matter

- UK workdays, accommodation history, or family connections that need to be checked against actual travel dates

- an arrival or departure year where split year treatment may matter

- the need to hand a clean factual timeline to an adviser instead of a rough estimate

At that point, the problem is not just arithmetic. It is record quality. One forgotten trip, one wrong departure date, or one prior-year gap can distort the analysis you or your adviser apply to the SRT.

How AtlasDays Helps

AtlasDays becomes useful when the Statutory Residence Test stops being a rough day-count question and becomes a travel-record problem.

It does not determine whether you are UK resident for tax purposes, and it does not decide whether a family tie, accommodation tie, work tie, or split year case applies. It gives you a cleaner dated travel record by country so you can review actual presence before applying HMRC guidance, checking the SRT tables, or handing your timeline to a professional adviser.

When UK residence questions stop being a guess

AtlasDays keeps a dated travel record by country so your UK timeline is cleaner before you apply the Statutory Residence Test or hand the facts to an adviser.

Get AtlasDays on the App Store